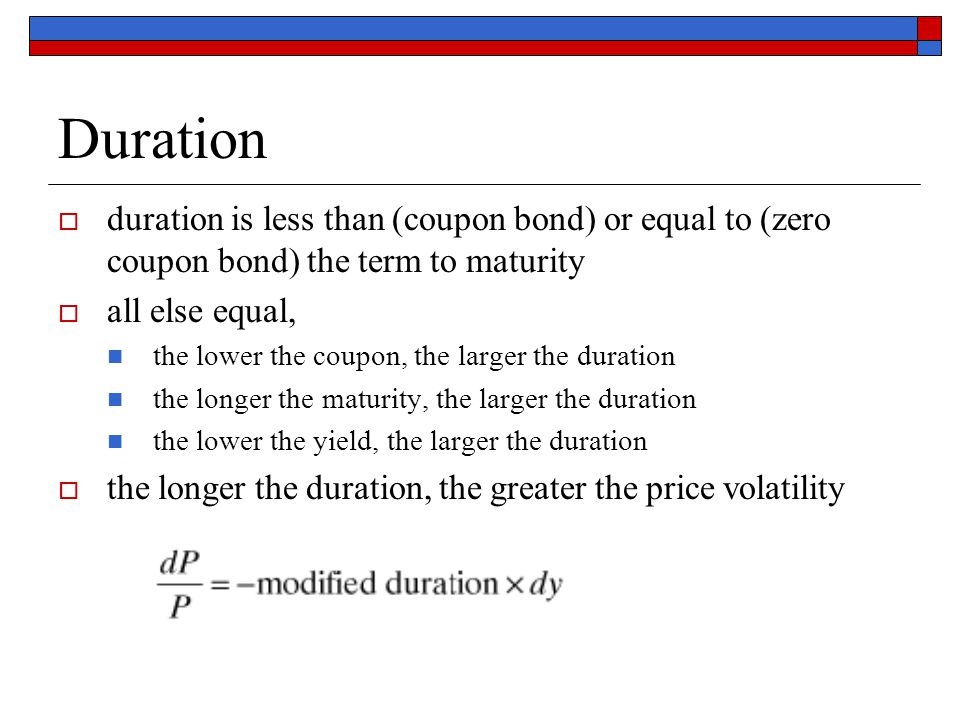

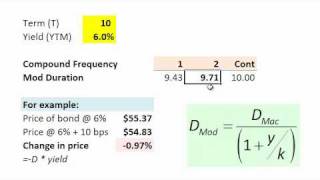

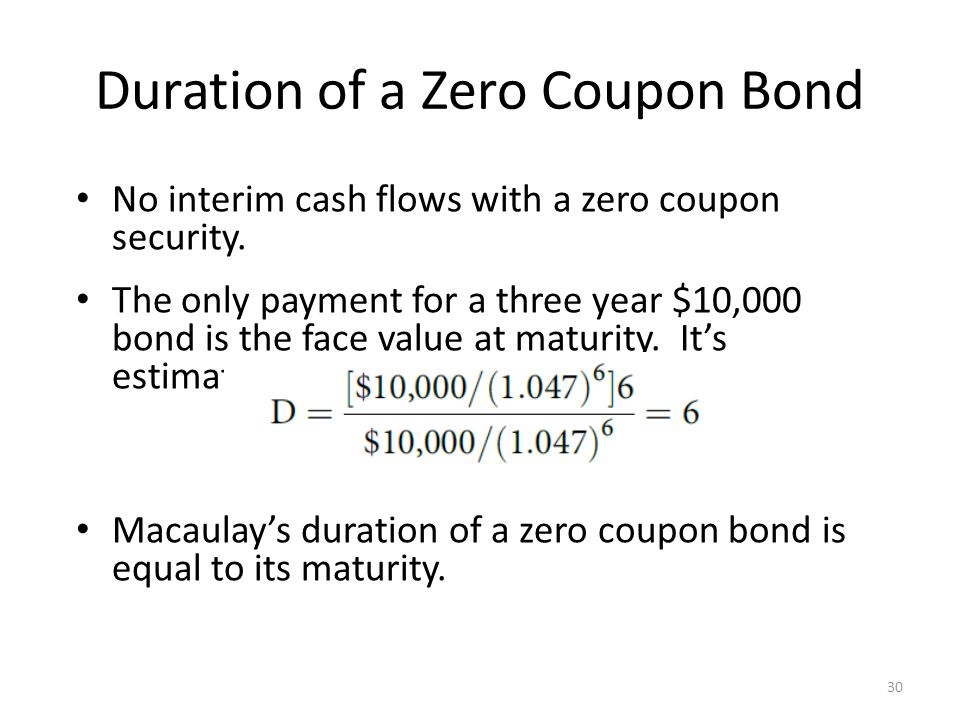

39 duration for zero coupon bond

Zero Coupon Bond Calculator - Nerd Counter How to Calculate the Price of Zero Coupon Bond? The particular formula that is used for calculating zero coupon bond price is given below: P (1+r)t; Examples: Now come to a zero coupon bond example, if the face value is $2000 and the interest rate is 20%, we will calculate the price of a zero coupon bond that matures in 10 years. Convexity of a Bond | Formula | Duration | Calculation The duration of the zero-coupon bond which is equal to its maturity (as there is only one cash flow) and hence its convexity is very high While the duration of the zero-coupon bond Zero-coupon Bond In contrast to a typical coupon-bearing bond, a zero-coupon bond (also known as a Pure Discount Bond or Accrual Bond) is a bond that is issued at a ...

Zero Coupon Bond Calculator – What is the Market Price? - DQYDJ P: The par or face value of the zero coupon bond; r: The interest rate of the bond; t: The time to maturity of the bond; Zero Coupon Bond Pricing Example. Let's walk through an example zero coupon bond pricing calculation for the default inputs in the tool. Face value: $1000; Interest Rate: 10%; Time to Maturity: 10 Years, 0 Months ...

Duration for zero coupon bond

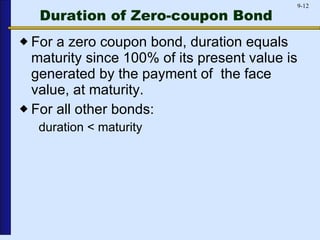

Bond valuation - Wikipedia Therefore, (2) some multiple (or fraction) of zero-coupon bonds, each corresponding to the bond's coupon dates, can be specified so as to produce identical cash flows to the bond. Thus (3) the bond price today must be equal to the sum of each of its cash flows discounted at the discount rate implied by the value of the corresponding ZCB. What Is the Macaulay Duration? - Investopedia Sep 29, 2022 · Macaulay Duration: The Macaulay duration is the weighted average term to maturity of the cash flows from a bond. The weight of each cash flow is determined by dividing the present value of the ... The Macaulay Duration of a Zero-Coupon Bond in Excel Aug 29, 2022 · The Macaulay duration of a zero-coupon bond is equal to the time to maturity of the bond. Simply put, it is a type of fixed-income security that does not pay interest on the principal amount.

Duration for zero coupon bond. Bond duration: how it works and how you can use it - Monevator Oct 25, 2022 · What is bond duration? Bond duration expresses a bond’s vulnerability to interest rate risk. The larger the bond duration number, the more reactive a bond’s price is to interest rate changes, as the bond’s yield adjusts to reflect those changes. For example, if a bond’s duration number is 11, then it: The Macaulay Duration of a Zero-Coupon Bond in Excel Aug 29, 2022 · The Macaulay duration of a zero-coupon bond is equal to the time to maturity of the bond. Simply put, it is a type of fixed-income security that does not pay interest on the principal amount. What Is the Macaulay Duration? - Investopedia Sep 29, 2022 · Macaulay Duration: The Macaulay duration is the weighted average term to maturity of the cash flows from a bond. The weight of each cash flow is determined by dividing the present value of the ... Bond valuation - Wikipedia Therefore, (2) some multiple (or fraction) of zero-coupon bonds, each corresponding to the bond's coupon dates, can be specified so as to produce identical cash flows to the bond. Thus (3) the bond price today must be equal to the sum of each of its cash flows discounted at the discount rate implied by the value of the corresponding ZCB.

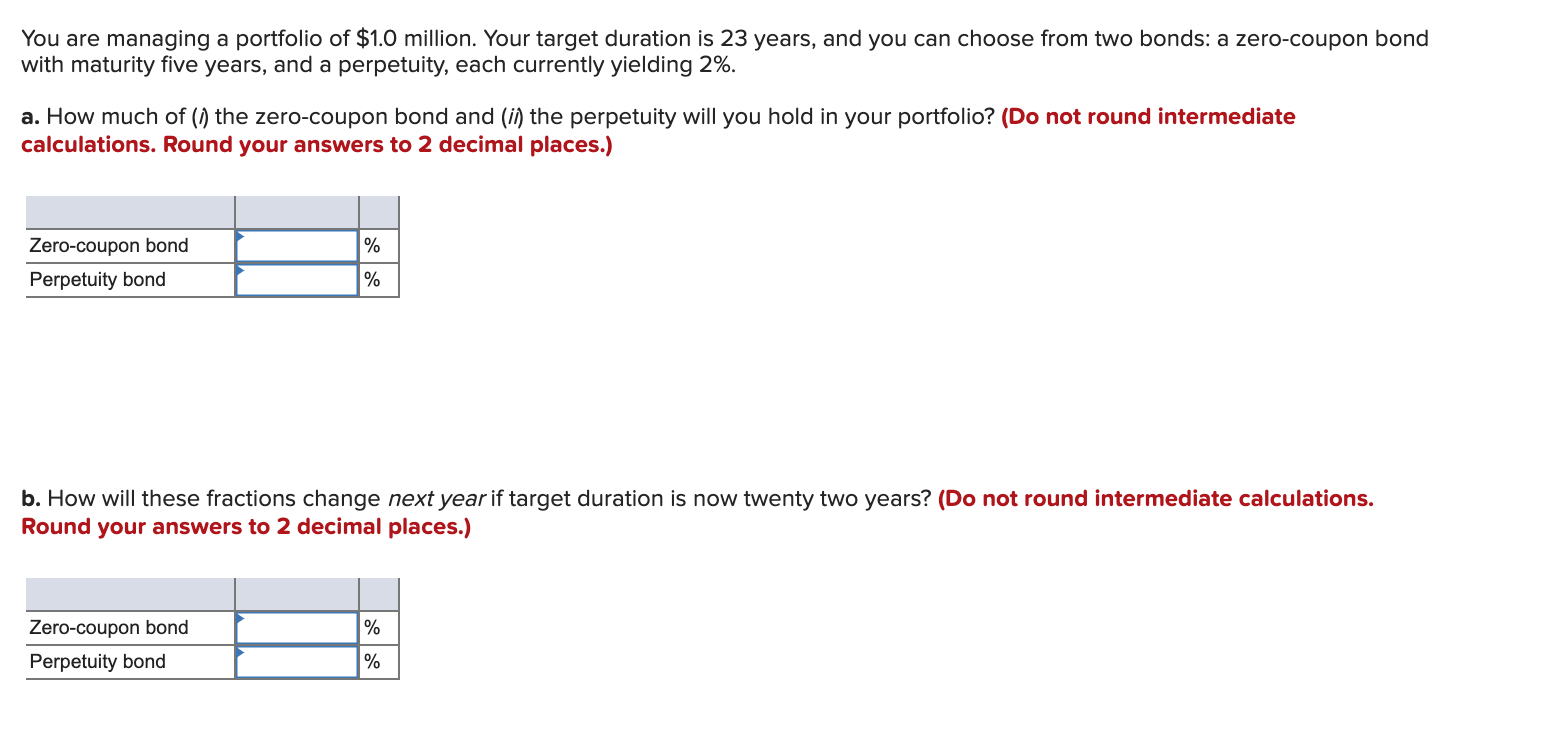

Solved You are managing a portfolio of $1.0 million. Your ...

:max_bytes(150000):strip_icc()/zero-couponbond_final-a6ec3618516a49c9a3654a1c79c9b681.png)

Zero-Coupon Bond: Definition, How It Works, and How To Calculate

Solved A 10-year zero coupon bond with a face value of ...

THE DURATION OF A BOND AS A PRICE ELASTICITY AND A FULCRUM

Zero Coupon Bond Valuation using Excel

Understanding Fixed-Income Risk and Return | IFT World

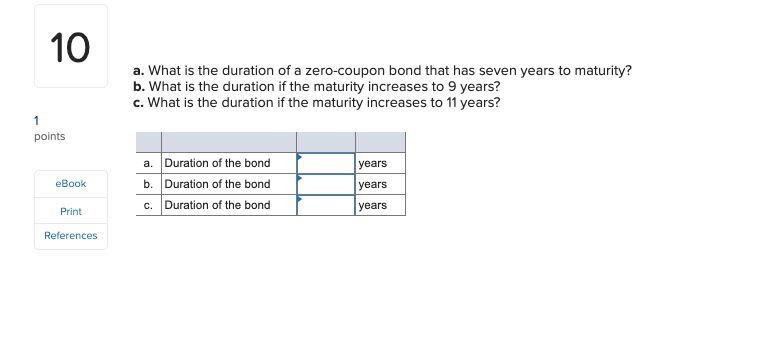

Solved a. What is the duration of a zero-coupon bond that ...

Solved a). What is the 1-year, 2-year, and 3-year spot ...

Zero-coupon bond - PrepNuggets

Zero-Coupon Bonds: Characteristics and Calculation Example

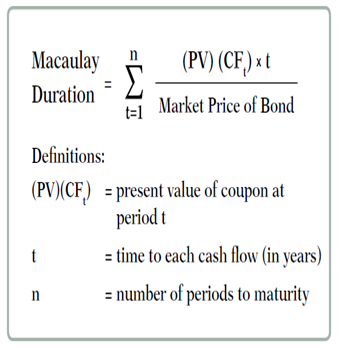

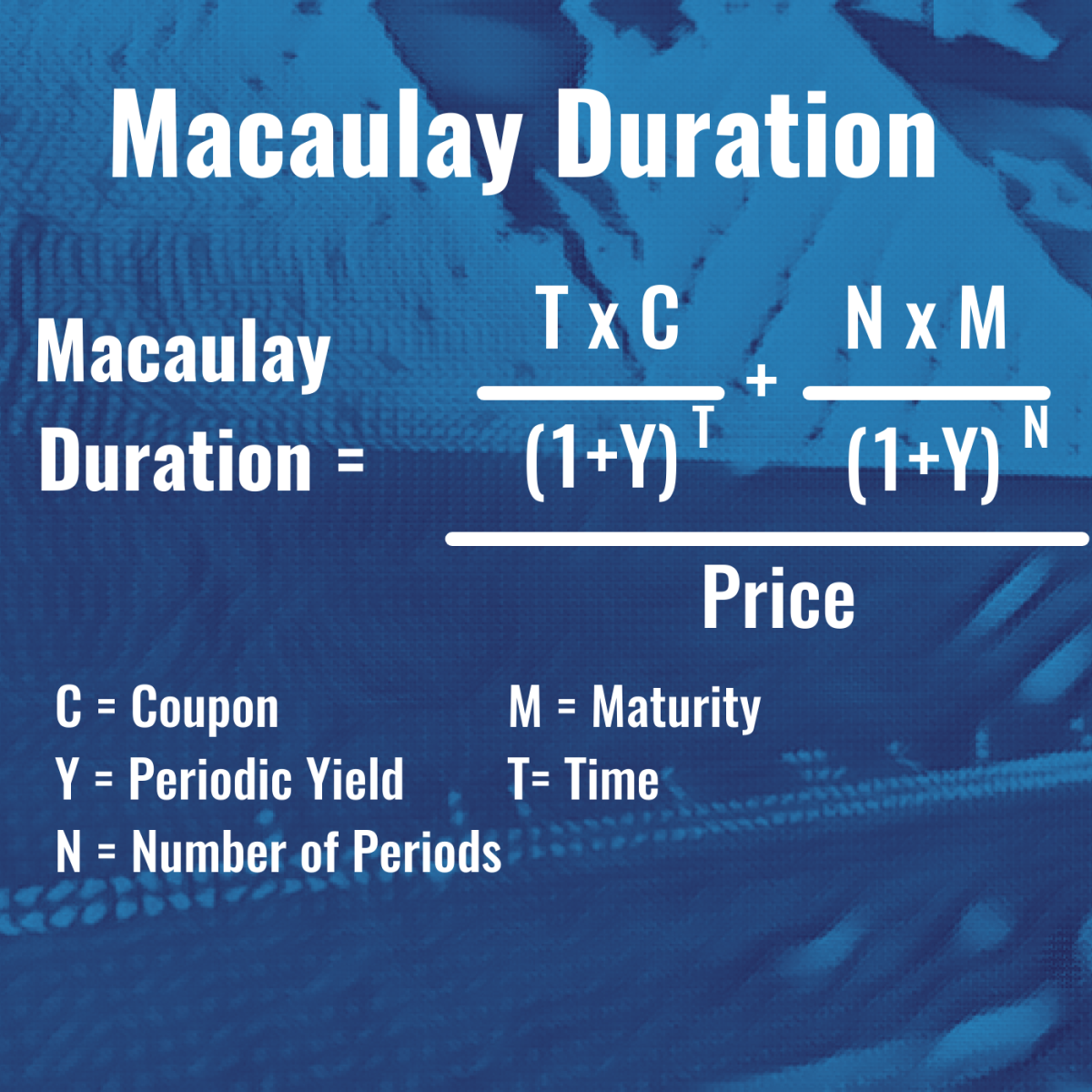

Macaulay Duration

![PDF] Duration and convexity of zero-coupon convertible bonds ...](https://d3i71xaburhd42.cloudfront.net/39b5487ce4f8becdfb0faf5ae6e30fd10537436c/13-Figure5-1.png)

PDF] Duration and convexity of zero-coupon convertible bonds ...

Reserve Bank of India - Database

Trading zero-coupon bond with maturity T = 5 years. Average ...

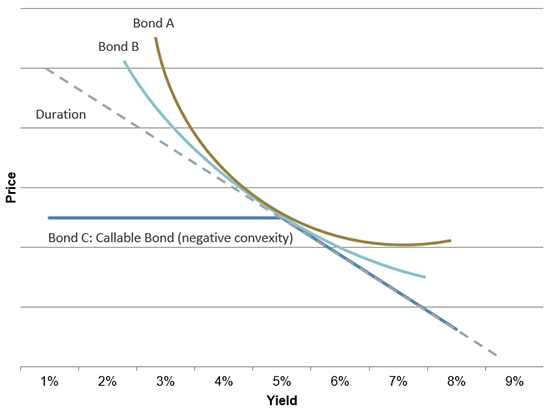

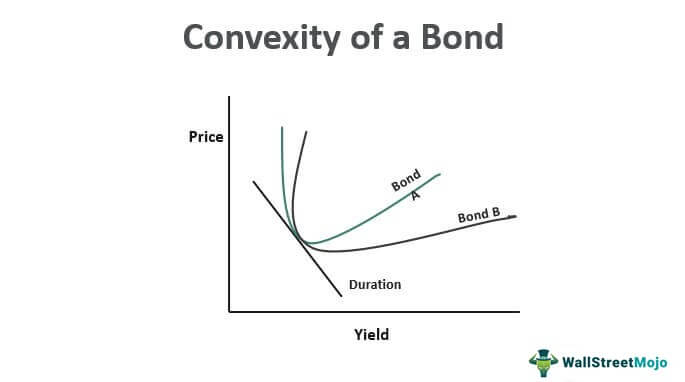

Convexity of a Bond | Formula | Duration | Calculation

A 12.75-year maturity zero-coupon bond selling at a yield to ...

Zero-Coupon Bond Definition & Meaning in Stock Market with ...

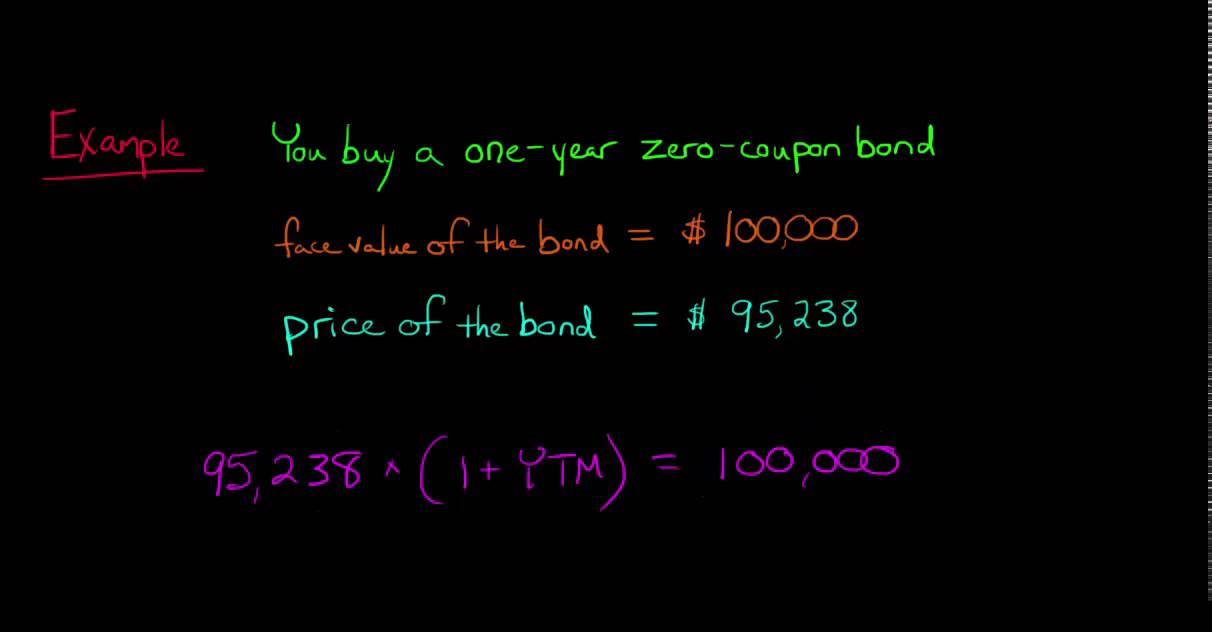

Calculating the Yield of a Zero Coupon Bond

Duration model

Duration & Convexity - Fixed Income Bond Basics | Raymond James

WWWFinance - Bond Valuation: Campbell R. Harvey

Solved] You are managing a portfolio of $3.0 million. Your ...

Duration Analysis

SOLUTION: Duration of zero coupon bond - Studypool

Bond duration - Wikipedia

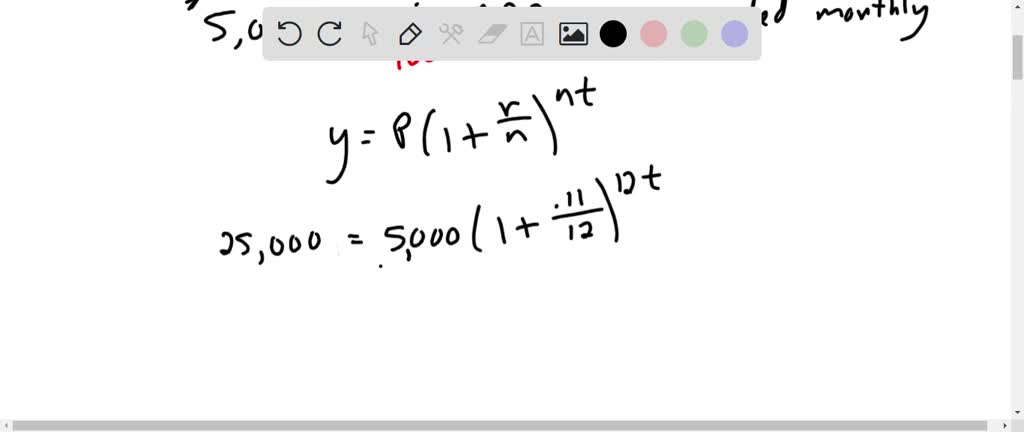

A zero – coupon bond can be redeemed in t years for 25,000. You, purchase this bond today for5,000 at 11% APR compounded monthly., When will this bond mature

Zero-Coupon Bond - Definition, How It Works, Formula | Wall ...

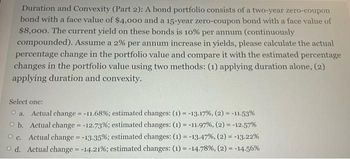

Answered: Duration and Convexity (Part 2): A bond… | bartleby

Convexity of a Bond | Formula | Duration | Calculation

Zero Coupon Bonds Explained (With Examples) - Fervent ...

Macaulay Duration

Chapter 4 Bond Price Volatility. - ppt video online download

How to compute the YTM of a zero-coupon bond - YouTube

Modified duration of zero-coupond bond (FRM practice question ...

Chapter 6: Pricing Fixed-Income Securities 1. Future Value ...

Solved You are managing a portfolio of $1.0 million. Your ...

Zero Coupon Bonds Explained (With Examples) - Fervent ...

What Is Duration of a Bond? - TheStreet Definition - TheStreet

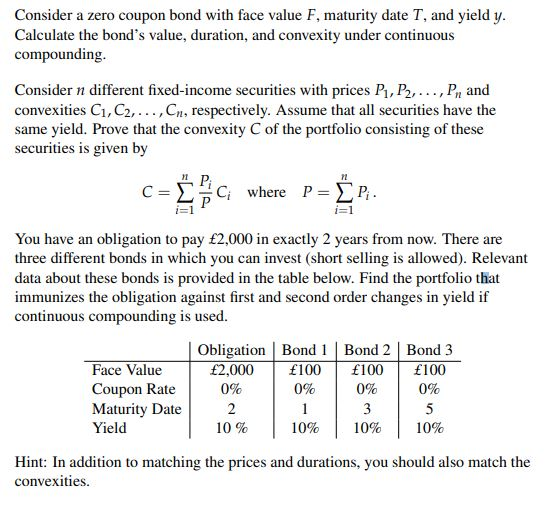

Consider a zero coupon bond with face value F, | Chegg.com

Post a Comment for "39 duration for zero coupon bond"